Detroit - Turn Back The Clock 100 Years

SEARCH BLOG: DETROIT

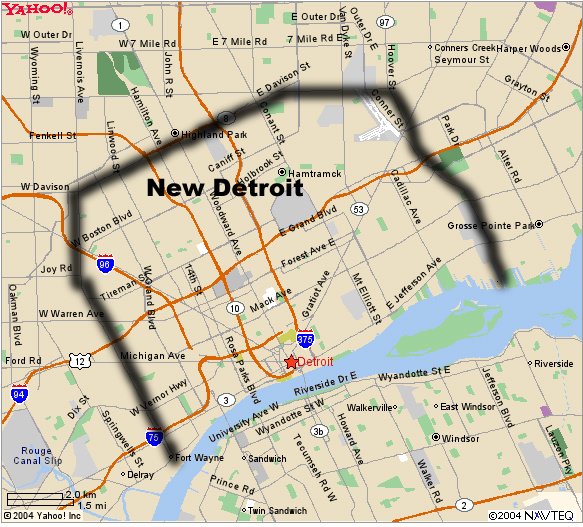

This blog is written in Michigan, so posts about Detroit are fairly frequent. Over the past half-dozen years, one concept has been put forth repeatedly: make Detroit's geographic area consistent with it's population.

This conceptual map has been shown many times. It is based on the common-sense approach that for Detroit to be viable, it must be supportable by the features that make most cities viable and be sized appropriately.

This conceptual map has been shown many times. It is based on the common-sense approach that for Detroit to be viable, it must be supportable by the features that make most cities viable and be sized appropriately.

This argument was once again proffered in light of Gov. Snyder's latest attempts to bring fiscal sanity to the city.

and...

As Michigan Recovers Detroit Spirals Into Oblivion

While this may seem far-fetched to many, the reverse would seem perfectly reasonable. Here is a map that shows Detroit's geographic growth:

So, why is no one else talking about the elephant in the room? Is it because Detroit is now a "black city" and one cannot deal honestly with "black cities?" Quite probably. One cannot raise the specter that a nearly all-black city has failed. Wouldn't be politically correct. Wouldn't be the first either.

But to be fair, here is an opposing view:

DETROIT (WWJ/1270 Talk Radio) – A community activist wants to see Detroiters who are on welfare become homeowners.

How? It’s a bold move, but Maureen Taylor with the Michigan Welfare Rights Organization said her group is hijacking empty bank-owned homes for those who are quickly running out of hope and resources.

“You can’t imagine,” Taylor said, “when we get to work at 9 and 10 in the morning, there are 20 to 30 people in the hallway talking about ‘I don’t have any more money, my rent is due’ — three or four months behind — what can I do? And, it’s unreal, because we don’t have answers except to say, ‘here’s a list of houses that we have intercepted that have been repossessed by banks, pick one and move in.’”

But what happens when banks catch on? As many are discovering with the backlog in foreclosed homes, it’s taking longer and longer for banks to actually repossess one.

“They have to take us to court, and by the way, the banks are picking up … it’ll take five or six to seven months before they figure out that we’re in there, and by that time, we will have taken hundreds of houses, if not thousands, so they can catch us if they’re fast enough.”

WWJ 950 legal analyst and Talk Radio 1270 host Charlie Langton said if and when the bank that owns the property finds out someone’s inside, it’s still not a criminal matter. “It’s a civil issue, it’s not a criminal act,” he said, adding banks could potentially find out the identity of the squatter and try to charge them for back rent and any damages to the property.

“But what are the chances they would do that?” Langton asked, adding that it’s not illegal to give out the addresses of abandoned homes.

It would be a bonus for the neighborhood, he added, if squatters would take care of the lawn and maintain the property.

“It is incumbent on the landowner to take pride in their property,” he said. “But in cases like this, the homeowner doesn’t care, they just let it go. They don’t care. That twisted logic is the real problem.”Yup, that's a plan to fix Detroit.

From

From